This is the first of a three-part blog series in which I will explain how and why commercial lenders and brokers should factor building efficiency into mortgage loans and property condition assessments. In this post, I’ll share some real-world examples of successful programs in the market that account for energy efficiency during mortgage underwriting and are paving the way to greater investment and savings.

Fannie Mae Shows Why Underwriting Energy Efficiency Works

A new market analysis performed by the Institute for Market Transformation (IMT) and the Lawrence Berkeley National Laboratory (LBNL) sheds light on trailblazers in the financial and real estate communities that are successfully marrying mortgage underwriting with energy efficiency. The commercial real estate market in particular, which accounts for 16 percent of U.S. emissions, has historically looked at mortgage loans and energy efficiency as mutually exclusive factors. However, underwriting additional loan proceeds based directly off of energy efficiency savings represents one of the most-sound financing options lenders can take, and could help reduce property default risks. Research shows that buildings whose mortgages include underwriting for energy efficiency see increased net operating income, reduced energy consumption, or increased energy savings.

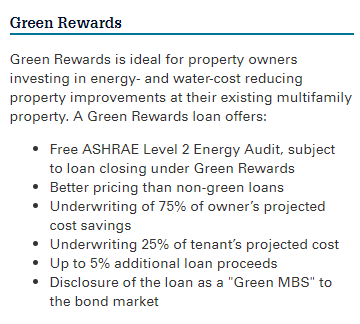

Right now, most of the available financing products and programs are limited to the multifamily sector. Perhaps the most developed energy and water efficiency financing option available to multifamily communities is the Green Rewards program run by Fannie Mae, one of the nation’s leading financial institutions. Throughout the second quarter of 2017, Fannie Mae created a $10.8 billion loan portfolio, up from $1.2 billion in 2016. Within this portfolio, multifamily properties that target a 20 percent or higher reduction in annual energy or water use are eligible to receive a lower interest rate, increased loan proceeds, and an energy audit to target improvements. This translates into large savings for both tenants who pay their own utility bills, and building owners who pay the mortgage or portions of tenant utility costs. The loans are issued to the market as Green Mortgage Backed Securities, creating a new investment vehicle for environmental, social, and governance (ESG) investors. IMT and LBNL believe this program offers a good model for a commercial and retail equivalent.

Right now, most of the available financing products and programs are limited to the multifamily sector. Perhaps the most developed energy and water efficiency financing option available to multifamily communities is the Green Rewards program run by Fannie Mae, one of the nation’s leading financial institutions. Throughout the second quarter of 2017, Fannie Mae created a $10.8 billion loan portfolio, up from $1.2 billion in 2016. Within this portfolio, multifamily properties that target a 20 percent or higher reduction in annual energy or water use are eligible to receive a lower interest rate, increased loan proceeds, and an energy audit to target improvements. This translates into large savings for both tenants who pay their own utility bills, and building owners who pay the mortgage or portions of tenant utility costs. The loans are issued to the market as Green Mortgage Backed Securities, creating a new investment vehicle for environmental, social, and governance (ESG) investors. IMT and LBNL believe this program offers a good model for a commercial and retail equivalent.

CPC Pioneers a New Sustainability Investment Method in New York City

Elsewhere, smaller community development financial institutions (CDFIs) are trying to integrate energy efficiency upgrades directly into mortgages. For example, the New York City-based Community Preservation Corporation (CPC) is a CDFI that pioneered a method of providing additional capital for sustainability improvements by incorporating future expense savings into the mortgage underwriting process. CPC provided construction and mortgage financing of $1.4 million for a 1920’s multifamily walkup located in New York City’s Washington Heights neighborhood.

The loan supported a roof-to-cellar renovation, which included new LED lighting, replacement of inefficient refrigerators with ENERGY STAR models, and a complete heating and domestic hot water system upgrade. As a result, the property reduced its annual utility costs by $23,000. Prior to the overhaul, the owner spent about $2,210/apartment on annual utility expenses. Post-retrofit that cost decreased to $1,540/apartment, representing an annual savings of roughly 30 percent.

The loan supported a roof-to-cellar renovation, which included new LED lighting, replacement of inefficient refrigerators with ENERGY STAR models, and a complete heating and domestic hot water system upgrade. As a result, the property reduced its annual utility costs by $23,000. Prior to the overhaul, the owner spent about $2,210/apartment on annual utility expenses. Post-retrofit that cost decreased to $1,540/apartment, representing an annual savings of roughly 30 percent.

As we see from these examples, the opportunity to incorporate efficiency into mortgages is clearly present in today’s market. Bridging the existing gap in commercial lending will require more education and better collaboration among many actors. Three parties in particular—traditional mortgage lenders (i.e. multinational banks and associated brokers), building owners, and tenants—all have the power to create major change and grow energy efficiency investment. What remains is for these parties to create a structured way to spread mortgage-level financing to tap into the vast potential.

In my next blog post, I will examine the important role of brokers in real estate transactions and how IMT’s broker education course is helping overcome the market failure that has resulted from lack of consideration for energy efficiency during underwriting. In my third and final post in the series, I will discuss the unique opportunity lenders have to increase mortgage loan portfolios, reduce property default risk, and provide a needed service to building owners by incorporating energy efficiency into building assessments, (I.E. property condition assessments or physical needs assessments). I’ll also offer a look at how innovative financing programs like the Small Business Association’s energy efficiency loan program is opening up new avenues for efficiency investment for small businesses across the U.S.

To download IMT and LBNL’s new analysis, click here.