In Part One of IMT and the Retail Industry Leaders Association’s (RILA) three-part blog series on external financing for energy efficiency, we highlighted our primers on traditional tools for larger retail projects such as Energy Performance Contracts (EPCs), Energy Service Agreements (ESAs), and Managed Energy Service Agreements (MESAs). For this post, we’ll take a look at Green Bonds.

Green bonds make a splash

To the financial market, bonds are nothing new. They’ve been used for centuries as a financing mechanism and investment tool, and retailers regularly use them to raise capital. However, as more businesses are seeking financing solutions specifically for energy efficiency and renewable energy projects, green bonds are making a splash in the marketplace. Early adopters have garnered substantial media interest and environmental groups are now calling for robust standardization as they gain popularity.

What are green bonds and who’s using them?

Green bonds are fixed-income instruments with funds earmarked for projects that advance climate change mitigation, energy efficiency, and other areas of sustainability. They are attractive to investors that value protecting the environment as well as companies looking for a simple and stable source of capital.

The proceeds from a green bond issuance can be used for a wide range of sustainability projects, making it ideal for retrofitting, constructing high-performance buildings, and accomplishing other major energy- and water-saving initiatives in the retail sector. Retailers can use green bonds to fund portfolio-wide projects, as issuances are typically at least several millions of dollars and can reach the billions. And unlike traditional energy efficiency financing, green bonds do not involve an energy service provider–giving retail companies autonomy over spending.

According to the Climate Bonds Initiative, the global aggregate of green bond issuances increased from approximately $11 billion in 2013 to $41 billion in 2015. Corporations were the second largest issuers of green bonds (after development banks) in 2014, responsible for 33 percent of total issuances. In 2016, the green bonds market is expected to top $50 billion and forecasts suggest the market will grow to over $1 trillion in annual issuances by 2020.

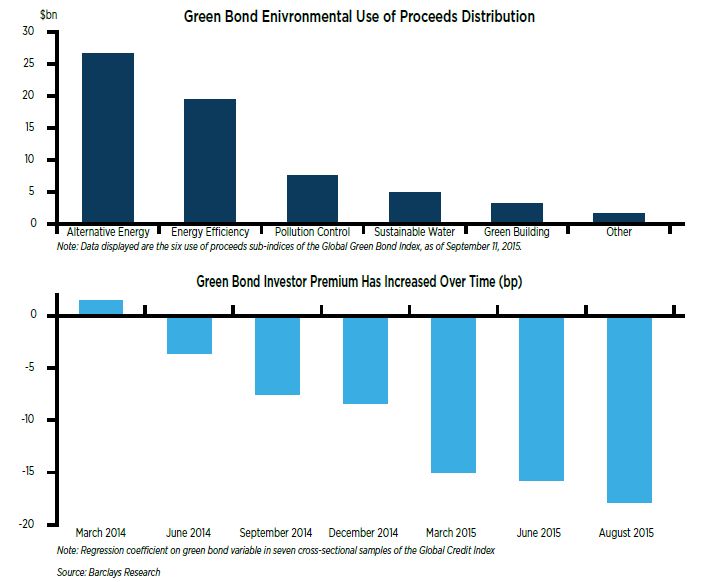

Click on the graphic to view IMT and RILA’s green bonds primer.

- In February, 2016, Apple issued $1.5 billion in green bonds. They plan to use the proceeds to fund renewable energy projects, as well as energy and water efficiency upgrades across its facilities, research and development into greener materials, and recycling and materials recovery projects. Goldman Sachs & Co., Bank of America, Merrill Lynch, Deutsche Bank Securities, and J.P. Morgan are managing Apple’s offering. Apple is committed to reporting about the allocations on an annual basis and has hired a third party verifier to conduct independent, annual updates about its progress.

- In May, 2016, Starbucks announced its first sustainability bond issuance. The company will use the net proceeds from the offering of $500 million to enhance its sustainability programs around coffee supply chain management. This includes coffee purchases from suppliers verified by a third-party as complying with their ethical sourcing verification program, the development and operation of farmer support centers in coffee growing regions, as well as short- and long-term loans. Starbucks will publish annual updates of the allocation of the proceeds throughout the term of the bond until the proceeds have been fully allocated.

Green Bonds: Are they for you?

For a retailer, the familiar structure of a bond offering combined with an innovative green spin make green bonds a promising way to raise capital for energy projects at favorable rates while attracting positive public attention for the company. Green bond proceeds can be used to advance energy and sustainability goals in retail stores, warehouses, distribution centers, and corporate offices, regardless of whether they are leased or owned.

Companies that are looking to do individual or small projects such as a lighting upgrade at a single facility would not be ideal candidates for green bonds. Other external financing options including PACE and On-Bill financing are better suited for small energy efficiency projects, which IMT and RILA will cover in our third and final post in this series. For more information on retail energy efficiency financing, visit RILA’s website to download our new resources for free.